Restaurant News: Champagne Sales Down -33%; PizzaExpress Closes 15% of Locations; Impressive Texas Roadhouse Earnings

Not the Year for Champagne Celebrations

Less party, less bubbly. Champagne bottle sales have fallen by one third during the first half of the year. Sales collapsed as low as -70% during May. Makers of the French wine say that they have foregone $2 billion in sales during the last six months. Because planning for grape production requires long lead times, vineyards estimate 100 million bottles will stay unsold even by the end of the year.

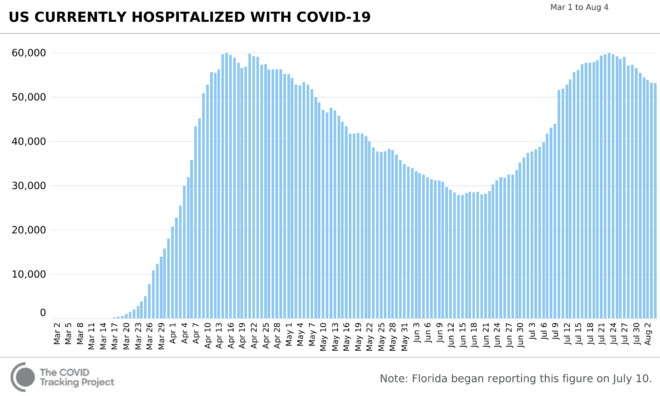

Today’s COVID-19 Numbers

There have been 47,576 new cases and 469 deaths in the U.S. since yesterday, bringing total domestic cases to 4.6 million. The country has 53,289 patients currently hospitalized with COVID-19.

Source: The COVID Tracking Project at The Atlantic (CC BY-NC-4.0)

Pizza Express

In the U.K., Pizza Express has announced a near-bankruptcy, “company voluntary arrangement” that will close 15% of its locations and lay off 1,100 workers. A company spokesperson says the layoffs are necessary to keep the company operational; “reducing the size of its estate will help it to protect 9,000 jobs.”

To get a better sense of Pizza Express’ finances, it is helpful to look at the company’s bond prices. Bond buyers are typically sophisticated investors. Unlike the stock market, the bond market is not dominated by retail traders. PizzaExpress’ $607 million worth of senior-secured notes closed the trading day at 59% of par value on Tuesday. The company’s $261 million lower-ranking bonds closed at just 3% of par value.

Texas Roadhouse

Back in the U.S., Texas Roadhouse (NASDAQ:TXRH) beat Wall Street analysts’ estimates by $0.14 per share, with revevenues in-line with estimates. The company’s Q2 (June) loss of $(0.48) per share was $0.14 better than analysts’ consensus of ($0.62) per share. Revenues for the quarter fell 30.9% versus Q2 2019 to $476.43 million versus Wall Street’s $474.75 million consensus estimate.

For the quarter, comparable store sales decreased -32.8% versus Q2 2019 at company restaurants, and -32.1% at domestic franchise restaurants. For April, May, and June, comps fell -46.7%, -41.9%, and -14.1%, respectively. The “improvement” from -46.7% to -14.1% was “positively impacted by the re-opening of dining rooms in a limited capacity in the majority of company restaurants.”

Although Texas Roadhouse traditionally offers forward guidance during its quarterly investor conference calls, it did not provide guidance due to the pandemic.

Following the upbeat earnings call, analysts at Telsey Advisory Group raised their TXRH price target to $64 from $50. Senior analyst Bob Derrington said, “Following its Q2 results, we have lifted our FY20 revenue, SSS and EPS, though have retained our FY21 EPS estimate at $2.25. Factoring a ~14x multiple to our revised higher FY21 EBITDA estimate, we have raised our PT to $64 (from $50), though have retained our MP rating reflecting the risk of more volatile sales trends as govt. support payments end.”

Texas Roadhouse has rallied 9% during the last five days, raising its one month gain to 14%.

Other analysts reiterated their positive outlooks. Today, Morgan Stanley maintained its Equal-Weight rating and $56 price target; Credit Suisse maintained its Outperform rating and $67 price target; Raymond James maintained its Strong Buy rating and $67.5 price target; and Stephens & Co. maintained its Overweight rating and $67 price target.

Leave a Reply